Despite being among the largest and fastest-growing segments of the healthcare industry, the biopharmaceuticals sector has historically lacked private equity sponsorship. The lack of early-stage profitability and the extreme drug-specific risk make acquiring pure-play biotech and biopharma companies a poor fit for financial sponsors' investment models. Companies that provide outsourced research and drug manufacturing for these companies, on the other hand, present compelling investment opportunities for private equity.

Scientific breakthroughs have resulted in a growing pipeline of drugs in development and robust demand for contract research organizations (CROs) and contract development and manufacturing organizations (CDMOs). Other ancillary areas in the broader biotech and biopharma ecosystem that present promising opportunities for financial sponsors include supply chain and automation, and data analytics.

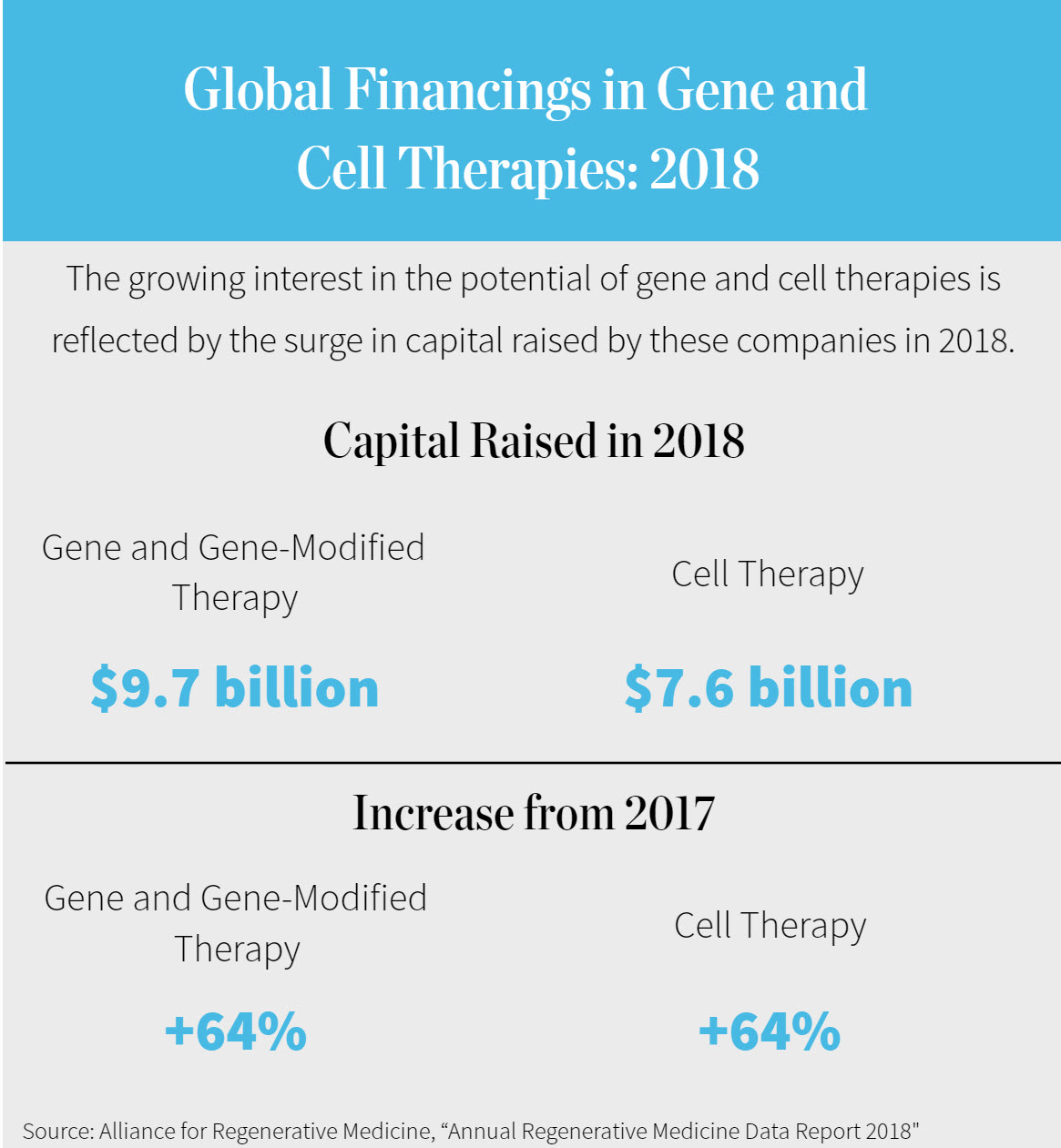

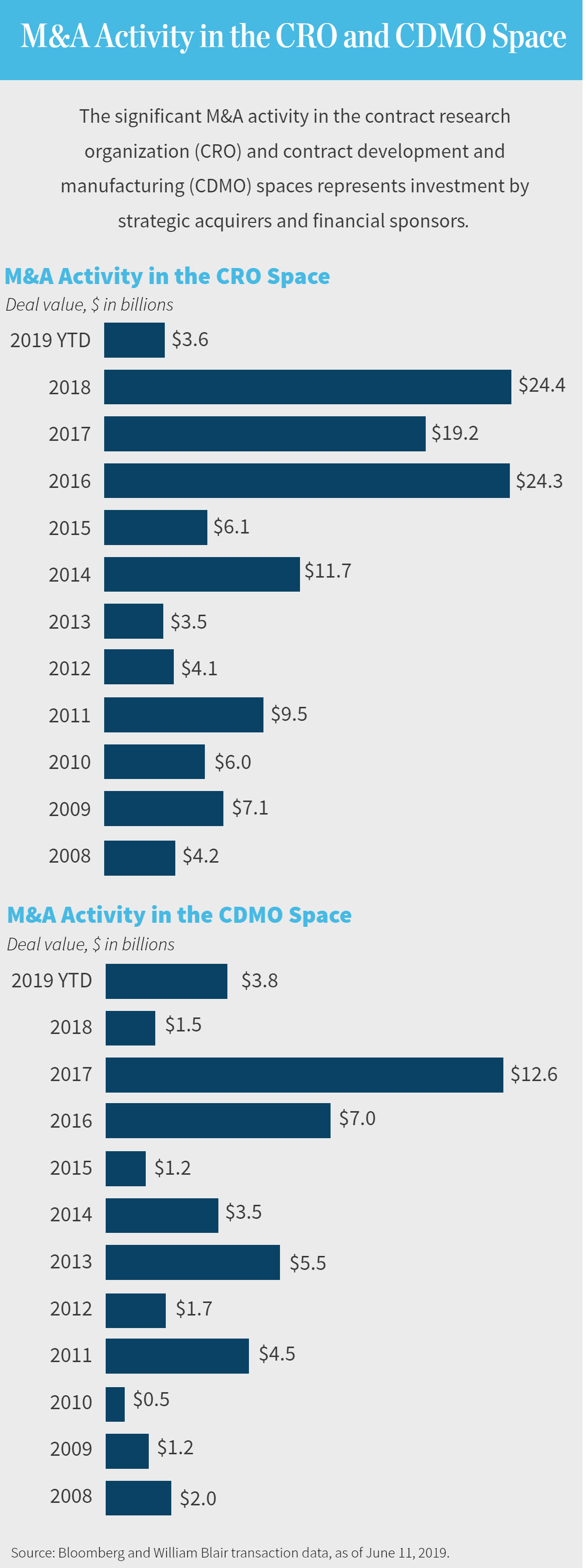

CDMOs, in particular, have seen an explosion in value creation over the past year. Thanks to rapid advancements in cell and gene therapy and a growing pipeline of biologic drugs in development, there is a significant shortage of manufacturing capacity and expertise for these products. This dynamic has led to strategic acquirers aggressively pursuing leading CDMOs such as Brammer Bio and Paragon Bioservices, both of which received robust valuations in their recent acquisitions.

We examine the trends that are driving the growth of outsourced services for biotech and biopharma and look at why financial sponsors should keep their fingers on the pulse of this vital sector.

Outsourcing Emerges as an Avenue for Private Equity Biotech Investment

Historically, there has been little private equity sponsorship of developmental-stage biotech companies. These companies have a long and uncertain path to profitability; the all-in cost of bringing a new drug to market, including post-approval R&D, was nearly $3 billion in 2013, according to researchers at Tufts University, Duke University, and the University of Rochester.¹ This business model is why biotech companies are funded almost exclusively by venture capital, crossover funds, and public equity.

CDMOs, CROs, and biotech suppliers have business models that are much more aligned with the investment horizons and risk appetites of financial sponsors. These companies can reach profitability after securing just a few key contracts, and CDMOs' largest expenses are manufacturing facilities that are fully capitalized.

It is important for financial sponsors to understand the scientific and regulatory trends that are driving value creation in the broader biotech and biopharma ecosystem, so investors don't overlook opportunities, like what has occurred with CDMOs and cell and gene therapy manufacturing recently. In December 2018, William Blair's equity research group hosted an event on the manufacturing aspects of engineered cell and gene therapies. It was heavily attended by investors, including financial sponsors that already own assets in the space as well as funds that are considering ways to participate in biotech.

Cell and Gene Therapy Pipeline Drives Surging CDMO Demand

Cell and gene therapies—two areas within the broader field of biologics, which are manufactured through complex processes that use large molecules—are one of the fastest-growing segments of the healthcare landscape. The management teams of Catalent and Thermo Fisher Scientific, the respective acquirers of Paragon and Brammer Bio, have noted that the market for contract manufacturing for cell and gene therapies is expanding at 25% annually.

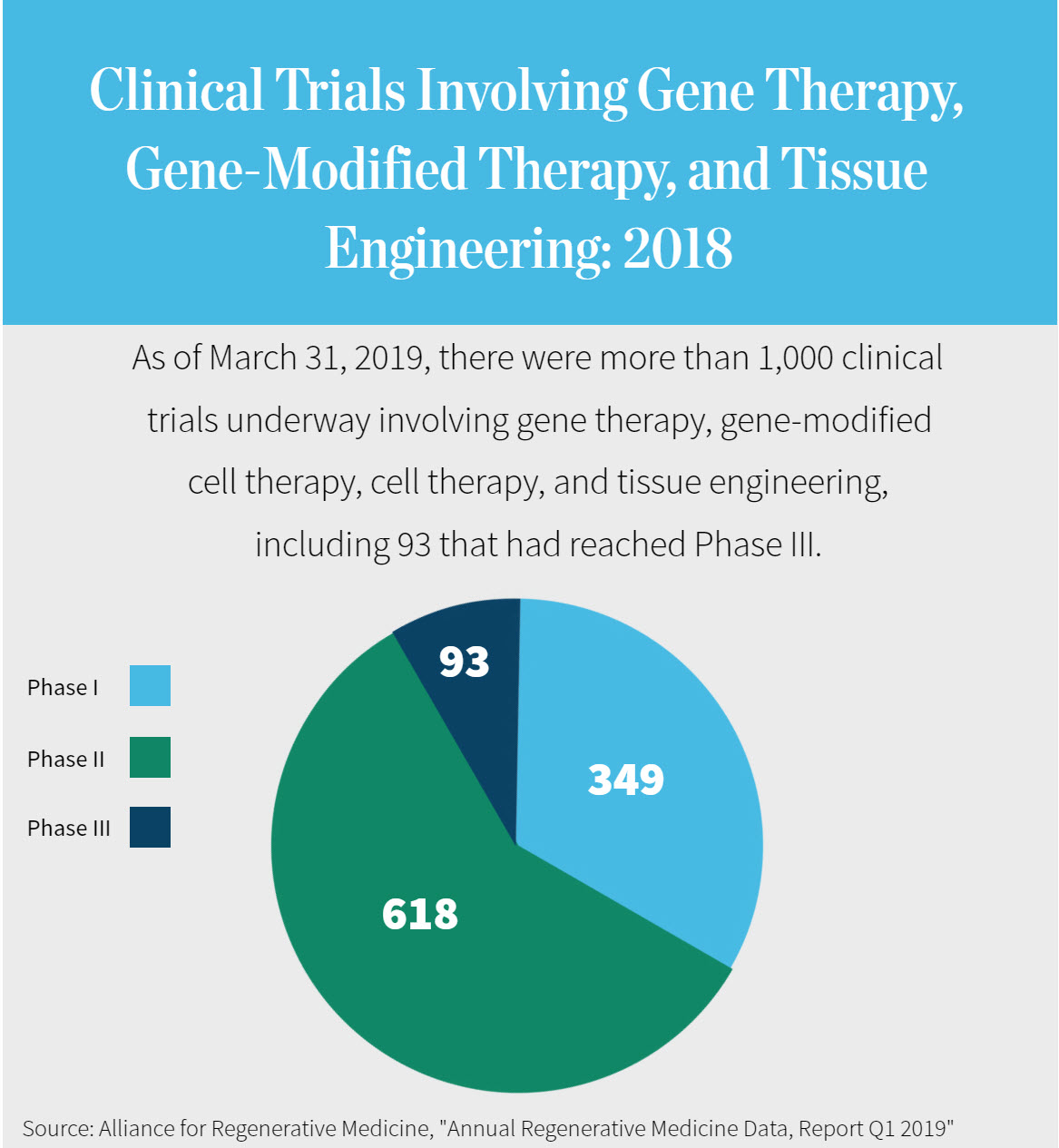

Clinical progress in cell and gene therapies has been very encouraging, with three recent FDA approvals, expectations for as many as 30 to 40 new drug approvals by 2025, and 680 new products under development. This growing pipeline is being fueled by scientific breakthroughs that have led to the development of drugs that have shown tremendous promise in treating cancer, monogenic diseases, and other severe illnesses.

Another tailwind to the growing pipeline of cell and gene therapies is a U.S. regulatory framework that is evolving to keep pace with the rapid innovation in biotech and biopharma. The 21st Century Cures Act, signed into law in December 2016, created the Regenerative Medicine Advanced Therapy designation, which is designed to speed the Food and Drug Administration's review of cell therapies and other products. This is part of the FDA's broader effort to reduce drug prices by streamlining the approval process and making it more transparent. These efforts are designed to bend the drug price curve downward by reducing the cost of drug development and increasing competition.

The rapid growth of the pipeline of cell and gene therapies, combined with the complex, unique requirements for producing these products, has created a severe shortage of manufacturing capabilities—and robust demand for CDMOs and suppliers that specialize in cell and gene therapy. The need for outsourced solutions is heightened by the fact that many of the new cell and gene therapies are being developed by small drug companies that don't have in-house manufacturing capabilities. These trends are also increasing demand for CROs—although the growth of the CRO market is less directly tied to cell and gene therapies specifically than is the case with CDMOs.

Paragon and Brammer Bio Headline Recent CDMO Transactions

These dynamics have resulted in significant value creation for CDMOs over the past several years, as these companies have drawn intense interest from strategic acquirers and financial sponsors. William Blair advised Paragon, a leader in viral vector contract manufacturing for gene therapies and a portfolio company of Camden Partners and NewSpring Health Capital, on its sale to Catalent for $1.2 billion, or 21.4x EBITDA. The transaction, which was announced on April 15, came a month after Thermo Fisher Scientific announced it was acquiring Brammer Bio, another leader in cell and gene therapy manufacturing and a portfolio company of Ampersand Capital Partners, for $1.7 billion.

Since 2017, William Blair has served as sell-side advisor to several CDMOs and CROs on transactions involving financial sponsors. Germany-based biotech firm Evotec acquired Aptuit, a portfolio company of Welsh, Carson, Anderson & Stowe, in August 2017. AGIC Capital and Humanwell Healthcare acquired The Ritedose Corporation, a portfolio company of Olympus Partners, in September 2017. Madison Dearborn Partners acquired Alcami, a portfolio company of Ares Capital, in July 2018.

In addition to our experience advising CDMOs and CROs, William Blair also has an extensive track record of providing M&A advisory and capital-raising services for biopharma companies. We advised Myonexus Therapeutics on its April 2019 acquisition by Sarepta Therapeutics. We served as an underwriter for Autolus Therapeutics, a cell therapy company, on its June 2018 IPO and its April 2019 follow-on offering, and we served as a joint book-running manager for Rocket Pharmaceuticals, a multi-platform gene therapy company, on its April 2019 follow-on offering.

To learn more about these and other trends that are shaping the dealmaking landscape in the biotech and biopharma industries, please don't hesitate to contact us.

¹DiMasi, Joseph; Grabowski, Henry; and Hansen, Ronald. "Innovation in the pharmaceutical industry: New estimates of R&D costs." Journal of Health Economics. January 2016.